Plasma: Stablecoin Supercycle

Disclaimer: This report was written in collaboration with Kairos Research. Kairos Research and ASXN have exposure to XPL. Additional disclaimers can be found at the end.

Introduction

Throughout history, money has consistently evolved to fulfill three core functions: as a medium of exchange, a store of value, and a unit of account, while a relentless drive for faster settlement, lower costs, and borderless usability has propelled its transformation from localized barter systems to today’s global digital networks. Stablecoins represent the next phase in the evolution of money and payments, forming the foundation of a financial system with faster settlement, lower fees, seamless cross-border functionality, native programmability and a strong auditability trail.

Dollar-denominated stablecoins are in high demand across a range of use cases (including store of value, remittances, payments, yield generation, and trading) and are increasingly being recognized by governments and treasury departments as strategic instruments. Beyond their utility in digital finance, they are emerging as tools of shadow monetary policy, used to manage sovereign debt and extend the reach of national currencies and financial systems globally.

With the backdrop of an improving regulatory environment, the evolving US debt situation and improving technology, we project stablecoin market cap to reach roughly $4.9 trillion over the next decade: nearly a 20x expansion from today’s levels.

Plasma is a purpose-built L1 optimized for stablecoins. As stablecoins continue to gain traction globally, we believe Plasma is well positioned to capitalize on this megatrend by delivering a highly tailored infrastructure for payments, remittances, on/off ramps, foreign exchange, and DeFi.

Stablecoins

Stablecoins are onchain representations of fiat currencies, most commonly the U.S. dollar. In essence, they wrap the dollar in software, allowing it to move anywhere the internet reaches, at the speed of light. Put simply, stablecoins are the fastest form of the dollar in existence. The market for these stablecoins has expanded from just $30 million in total market cap in 2018 to >$250 billion today, representing a 263% compound annual growth rate. Initially used as crypto-native collateral and a settlement mechanism, particularly by market makers and arbitrageurs,stablecoins have since evolved into a broadly adopted financial primitive.

Today’s stablecoin landscape consists of several distinct types of stablecoin, primarily differentiated by their collateral backing, degree of decentralization, and the mechanism used to maintain their peg. Fiat-backed stablecoins dominate the market, accounting for over 92% of total stablecoin market capitalization. We segregate them into the following categories:

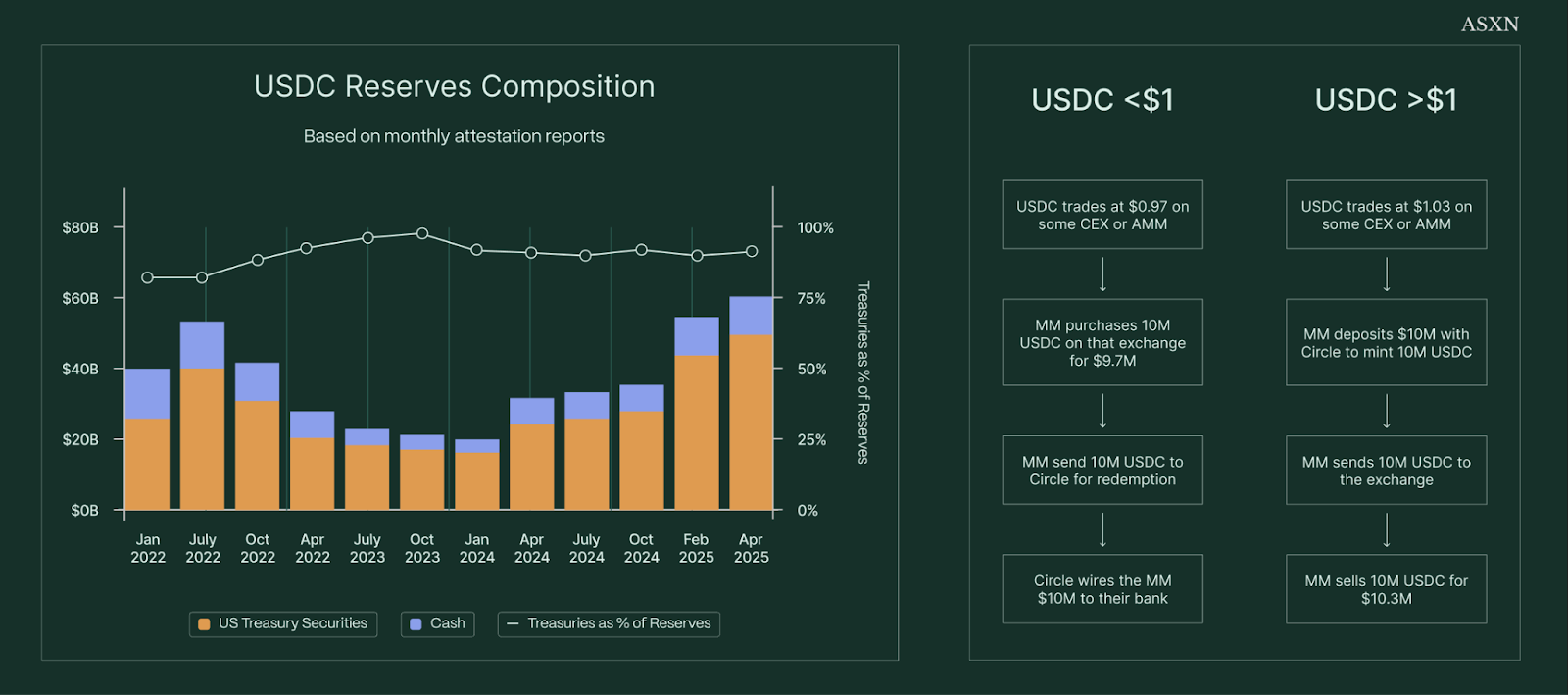

Fiat Backed - A fiat-backed stablecoin maintains its 1:1 peg by fully collateralizing each digital token with an equivalent amount of fiat currency held off-chain. For example, each USDC token is backed by $1 held in a combination of cash and short-term U.S. government debt. According to current reserve disclosures, each 1 USDC is supported by approximately $0.885 in U.S. Treasuries and $0.115 in cash. Select entities can mint and redeem fiat-backed stables, enabling arbitrage to keep the token pegged to $1. Fiat-backed issuers derive most of their revenue from deploying their reserves into interest-bearing US debt instruments. For instance, Tether earned approximately $7 billion in 2024 from holdings in U.S. Treasuries and repo agreements.

Crypto-backed - Crypto-backed stablecoins operate similarly but mostly utilise overcollateralized lending systems due to their decentralised / non-KYC nature. Typically, a user deposits collateral,such as $1,000 worth of BTC,into the protocol, which then mints up to $800 in stablecoins, reflecting an 80% loan-to-value (LTV) ratio. To protect the system from insolvency in the event of collateral depreciation, the protocol enforces liquidation thresholds. If the collateral value falls below a specified LTV ratio, the system automatically liquidates the user’s BTC to cover the outstanding debt, thereby preventing the accumulation of bad debt. This closely mimics how banks create new money through lending but with liquid, on-chain collateral.

Algorithmic - As opposed to fiat-backed and crypto-backed stablecoins, algorithmic stablecoins are not always backed by hard assets and instead rely on algorithms and smart contracts to maintain the peg. Seigniorage, or dual-token, algorithmic stablecoins use a two-token system to stabilize value. The other two categories are rebasing stablecoins, which adjust wallet balances directly to maintain a $1 peg (e.g., Ampleforth/AMPL), and fractional algorithmic stablecoins, which combine partial collateral (e.g., USDC, ETH) with algorithmic supply controls, as in early versions of FRAX. Under current US regulations and the GENIUS compliance Act, algorithmic stablecoins are essentially banned.

Strategy-backed - A new category of “stablecoins” has recently emerged,tokens that maintain a $1-denominated value while embedding exposure to yield-generating investment strategies. These instruments function less like traditional stablecoins and more like dollar-denominated shares in an open-ended hedge fund. The concept gained attention in March 2023 when Arthur Hayes, founder of BitMEX and a pioneer of the perpetual future contract, published Introducing the NakaDollar, which later manifested itself as the USDe stablecoin by Ethena. We refer to these strategy-backed stablecoins as a dollar product, or synthetic dollar product throughout, but it is important to note that they have a different risk profile to what many consider to be a traditional stablecoin.

Beyond the different categories of stablecoin issuers, a rapidly expanding ecosystem is emerging to support them: powering P2P, B2B, and B2C payments, orchestration, foreign exchange, payroll, consumer banking, and card issuance.

Stablecoin Use Cases

Store of Value

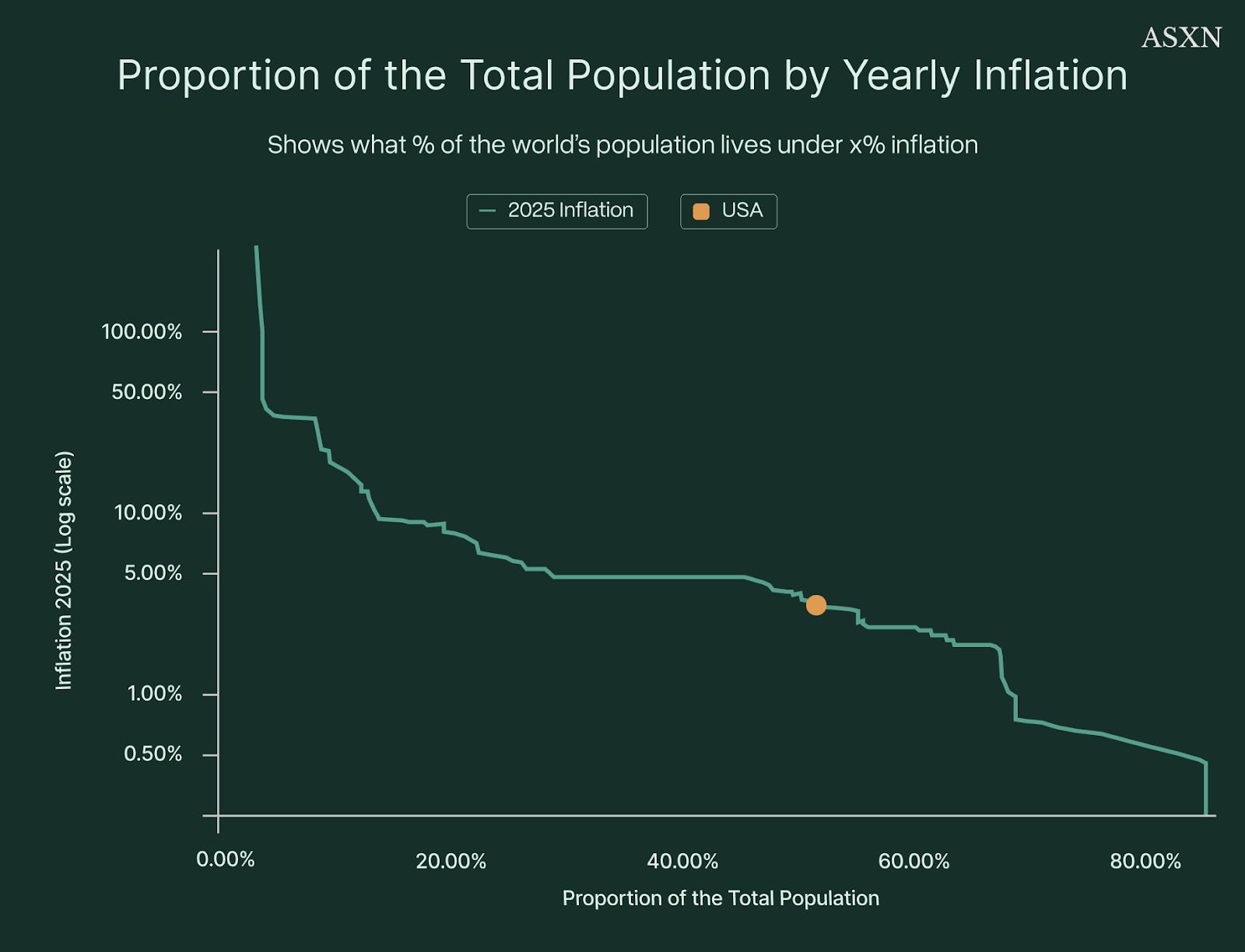

While most investors, particularly those in Bitcoin, recognize that the U.S. dollar is slowly losing purchasing power due to persistent inflation and currency debasement, as Ray Dalio aptly puts it, “the dollar is still the least dirty shirt in the hamper.” In fact, over 20% of the global population lives under regimes experiencing inflation rates of 6.5% or higher and over 51% live with worse inflation than in the USA (in 2025). In countries grappling with runaway inflation, weakening currencies, or strict capital controls, a grassroots financial shift is underway: individuals and businesses are increasingly turning to USD-pegged stablecoins as a store of value. Rather than hold rapidly depreciating local currencies, people in economies like Argentina, Turkey, Lebanon, Venezuela, and Nigeria are parking savings in digital dollars such as USDT, USDC, or DAI. In these environments, stablecoins function less as payment rails and more as digital savings accounts,offering a more stable alternative for preserving purchasing power. You can read more about this use case in our article on store of value here.

Remittance

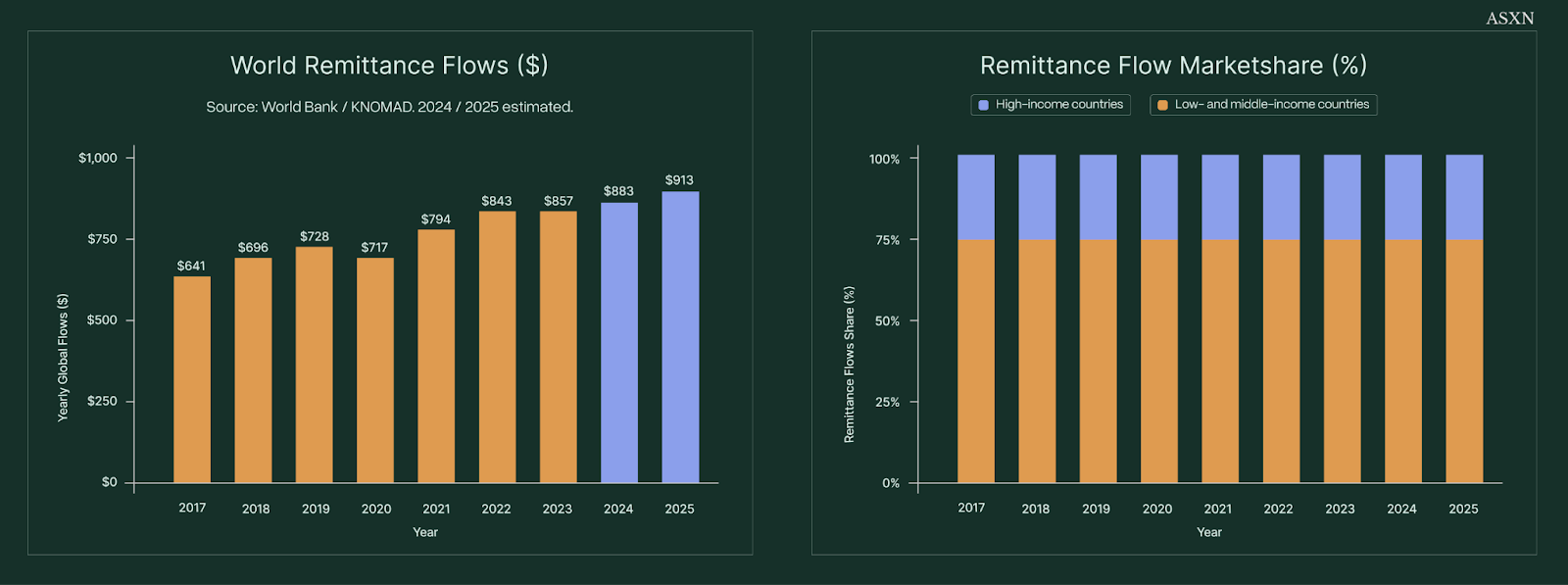

Remittances represent a major use case for stablecoins. Each year, tens of millions of workers send a portion of their wages back home, supporting over 200 million recipients globally. In 2024, total remittance flows reached approximately $905 billion, a figure comparable to the GDP of a mid-sized developed economy. Continued growth is expected in 2025. A substantial share of these flows, around 76 percent or an estimated $685 billion, went to low and middle income countries (LMICs), where remittances often serve as a financial lifeline.

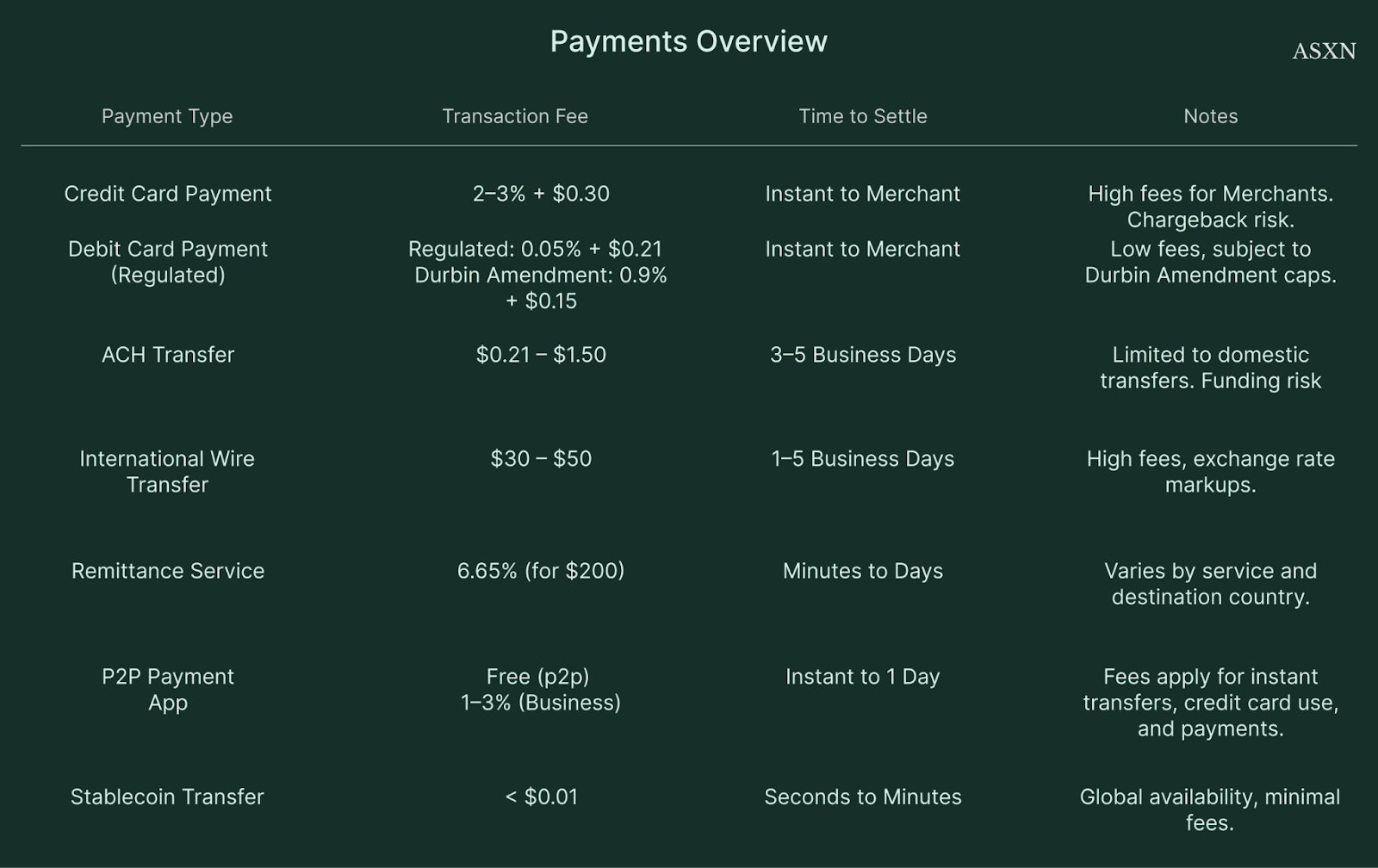

In the fourth quarter of 2023, the average cost to send $200 abroad was approximately 6.4 percent. In some corridors, that number exceeded 10 percent. For people already managing tight budgets, losing such a large portion of a remittance to fees can be a significant burden. These costs act like a regressive tax on some of the world’s poorest workers and despite the 2030 Sustainable Development Goal of reducing global remittance costs to 3 percent, fees have continued to rise, increasing by 3.2 percent year over year.

Just as the internet revolutionized information by enabling it to travel globally at the speed of light, stablecoins are doing the same for value transfer. Stablecoins and the crypto rails they run on offer an internet-native alternative for moving money, optimized for speed, transparency, and low cost. Plasma will enable zero transfer fees on USDT transactions, creating both one of the fastest dollars in the world, but also the cheapest. Stablecoins are well suited for remittances not only because they provide a more stable store of value (in digital dollars), but also because they benefit from the efficiency and settlement benefits of transferring value on blockchain rails.

Payments

While remittances form a distinct subsegment, the broader global payments ecosystem (which spans consumer-facing transactions, business-oriented flows, public-sector and social disbursements, as well as emerging and embedded rails) continues to grapple with legacy infrastructure. Core limitations such as high costs, slow settlement times, limited transparency, and poor composability persist across all segments. Yet despite these structural inefficiencies, the global payments industry remains one of the largest in the world, processing 3.4 trillion transactions in 2023, representing $1.8 quadrillion in value and generating $2.4 trillion in revenue.

A16Z offers a comprehensive overview of these traditional payment methods, detailing their associated fees, settlement times, and operational nuances. Compared to crypto rails, these legacy systems appear outdated: characterized by higher transaction costs, slower settlement, chargeback risks, closed networks, and limited accessibility.

In our view, the most immediate impact from stablecoin-based payments will be felt by U.S.-based companies, particularly those selling into the world’s largest consumer market: the United States itself. This is largely due to the high prevalence of credit card usage and the associated processing fees in the U.S.

Crypto Trading

As we highlighted in our stablecoin overview, these tokens first gained traction as crypto-native collateral and settlement rails: powering market makers and arbitrageurs to optimize capital efficiency. Today, trading firms and liquidity providers carry substantial stablecoin balances, while DeFi protocols embed them across collateral vaults, lending pools and AMM pairs. Centralized exchanges have likewise shifted their perpetual futures from BTC- or crypto-collateralized margining to stablecoin-based contracts (predominantly USDT pairs (with USDC fast growing)) which now dominate trading volumes and liquidity depth. Off-exchange, OTC desks routinely settle large trades in stablecoins, and USD-denominated tokens have become the preferred unit of account for market-neutral and crypto credit/yield funds.

Yield Generation

Beyond serving as a reliable store of value and a frictionless payment medium, stablecoins unlock permissionless access to a variety of yield-generating strategies: an especially significant benefit for investors shut out of traditional markets, including U.S. capital markets.

Monetary Policy

Stablecoins are also emerging as powerful instruments of shadow monetary policy, increasingly recognized by governments and treasury departments as strategic tools to manage sovereign debt and proliferate currency and financial system strength around the world. In Washington, this use case is moving to the forefront as the U.S. government seeks innovative ways to control its debt burden.

The mechanism through which stablecoins can help lower the government’s cost of borrowing operates as follows:

As outlined in the stablecoin category section, fiat-backed stablecoins typically allocate the majority of their reserves to short-term U.S. government debt instruments: primarily Treasury bills and reverse repurchase agreements. This strategy allows centralized issuers to earn yield on customer deposits, either as a revenue source or, in some models, to pass through to stablecoin holders.

It follows that as the market capitalization of fiat-backed stablecoins grows, demand for short-term U.S. government debt should increase in roughly linear proportion. Reserve disclosures from leading issuers support this trend: Tether and Circle currently hold the vast majority of their assets in government-backed instruments. Circle reports that 88.5% of its reserves are held in U.S. Treasuries, while Tether holds approximately 82.2% in a combination of Treasuries, repo agreements, and money market funds.

This additional demand for government debt puts upward pressure on bond prices, which (given the inverse relationship between price and yield) results in lower yields. As a result, the U.S. government can borrow at lower interest rates, reducing the cost of financing its operations.

The US national debt is reaching unprecedented absolute levels and record highs relative to GDP, with peacetime budget deficits of a magnitude never previously seen. This dynamic is driving a compounding increase in the overall debt burden. At the same time, traditional buyers of US Treasuries (such as foreign central banks and reserve managers) have materially reduced their demand, leaving relative value (RV) hedge funds as the marginal buyers setting prices at the margin. However, this mechanism is increasingly fragile. A notable example was during the post-Trump tariff war period, when many RV funds were rumored to have suffered significant losses, contributing to rising 10-year yields even as equity markets sold off. We discuss this more in our stablecoin report here.

TAM of Stablecoins

Stablecoins serve a wide range of functions, depending on the user. For individuals in autocratic or high-inflation regimes, they provide a self-custodial store of value and a means of preserving wealth. For others, they offer a fast and low-cost way to send money across borders to family and friends. For companies, stablecoins act as financial “superconductors,” enabling instant, 24/7 cross-border settlement at a fraction of the cost of traditional payment systems (directly improving efficiency and margins. And for governments) particularly the U.S. government: stablecoins are emerging as potent tools of shadow monetary policy, extending financial influence and dollar strength globally while also creating a new source of demand for U.S. sovereign debt. Stablecoins therefore touch many markets and segments and estimating the TAM or market capitalization growth of stablecoins requires a lot of assumptions.

By aggregating the major immediate use cases for stablecoins and applying reasonable assumptions for adoption levels across each (10% here), we can begin to estimate the potential scale of stablecoin supply as adoption grows. Focusing specifically on offshore USD demand, remittances, payments, and MMF substitution, our analysis suggests stablecoin supply could grow to approximately $4.9 trillion with modest levels of penetration.

This market capitalization would of course grow linearly with increasing levels of market penetration in each segment, not with counting the more speculative use cases of stablecoins such as AI native payments.

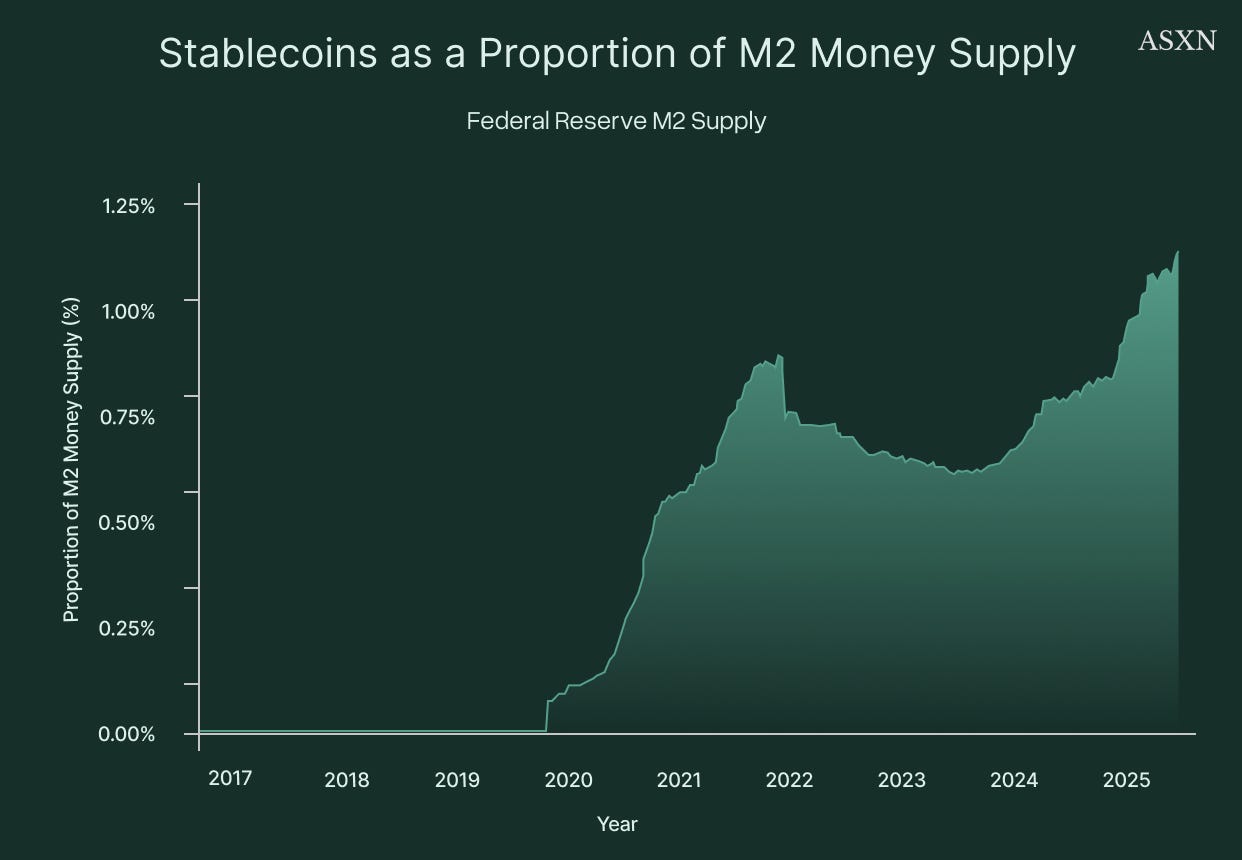

M2 (the broadest commonly cited measure of the U.S. money supply) comprises all of M1 (currency in circulation and checking deposits) plus “near-money” instruments such as savings deposits, small time deposits (under $100,000) and retail money-market funds. As of today, M2 stands at approximately $21.86 trillion, of which stablecoins account for just over 1.1 percent. With clearer regulatory guidelines, more robust infrastructure and the ongoing shift toward fully digital payments, we believe that stablecoins’ share of M2 could grow tenfold over the next ten years.

Plasma

Plasma combines a Byzantine Fault Tolerant (“BFT”) consensus protocol, PlasmaBFT, with an execution layer built on Reth. The chain is EVM-equivalent, meaning contracts, opcodes, and tooling behave the same as Ethereum. On top of EVM-equivalency, the chain adds stablecoin-native features at the protocol level: zero-fee USD₮ transfers and support for custom gas tokens.

PlasmaBFT

HotStuff Background

Hotstuff was created by VMresearch and further enhanced by LibraBFT from Meta’s former blockchain team. It achieved both linear view change and responsiveness, meaning it can efficiently rotate leaders while progressing at actual network speed rather than predetermined timeouts. HotStuff also uses threshold signatures for efficiency, and implements pipelined operation allowing new blocks to be proposed before previous ones are committed.

However, these benefits come with certain tradeoffs: an additional round compared to classic two-round BFT protocols leads to higher latency and the possibility of forks during pipelining. Despite these tradeoffs, HotStuff’s design enables better scaling, making it particularly suitable for large-scale blockchain implementations, even though it results in slower finality than two-round BFT protocols.

Below is a simplified breakdown of HotStuff:

When transactions occur they are sent to one of the network’s validators, known as the leader.

The leader compiles these transactions into a block and broadcasts it to the other validators in the network.

The validators then verify the block by casting their votes, which are sent to the leader of the next block.

To safeguard against malicious actors or communication failures, the block must undergo multiple rounds of voting before the state is finalized.

Depending on the specific implementation, the block is only committed after successfully passing through two or three consecutive rounds, ensuring consensus is robust and secure.

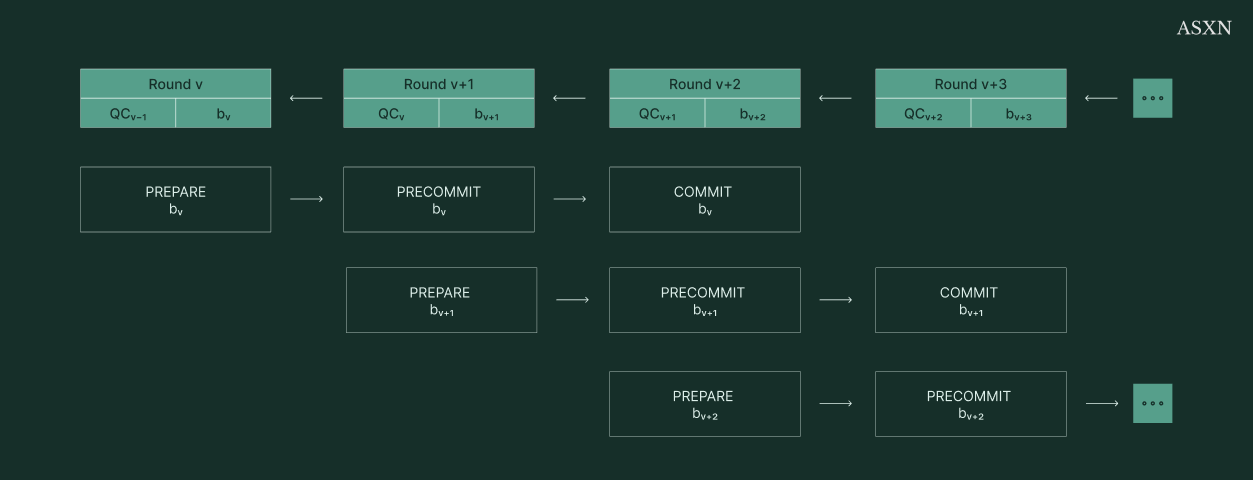

PlasmaBFT Design

Compared to regular HotStuff, PlasmaBFT implements a few changes. PlasmaBFT is a pipelined implementation of Fast HotStuff written in Rust. The protocol guarantees that two conflicting blocks cannot both be finalized, as long as fewer than a third of validators are faulty. To finalize a block, at least two thirds of validators have to approve it. Because the two thirds groups always overlap, there will always be honest validators in common, and they will not sign conflicting blocks.

In the fast path, PlasmaBFT uses a two-chain commit rule so blocks can finalize after two consecutive quorum certificates instead of three. Pipelining allows leaders to propose new blocks before previous ones are finalized.

PlasmaBFT aggregates validator votes into quorum certificates (QCs). A QC is proof that a supermajority of validators approved a block. Validators sign the block if they agree, and when at least two thirds of votes are collected, those signatures are combined into a single certificate.

QC creation works as follows:

The leader proposes a block.

Validators vote by signing the block.

Once two thirds of votes are collected, they are aggregated.

The result is a QC, which proves the block is safe to extend.

During a view change, validators send their latest QC to the new leader. The new leader aggregates these into an aggregated quorum certificate (AggQC). The AggQC shows, in one object, the highest block that a supermajority considers safe. This prevents forks during leadership changes and reduces overhead by compressing many signatures into a single proof.

PlasmaBFT also differs in how it handles incentives. Instead of stake slashing, it uses reward slashing.In a stake-slashing system, if a validator misbehaves (double-signs, censors, goes offline), part of their staked capital is destroyed. This creates strong security but also high risk, since even accidental mistakes can cost a validator real funds.

In PlasmaBFT, misbehavior or non-participation does not burn the validator’s stake. Instead, the validator just doesn’t earn rewards for that period. Rewards are distributed only to validators who actively participate and follow the rules. If validators fail to sign blocks, sign conflicting blocks, or miss your duties, they don’t earn rewards.

PlasmaBFT does not have every validator vote on every block. Instead, it forms a smaller committee for each round. Committees are chosen using a stake-weighted random process. Committees reduce latency and reduce communication costs, as only the committee needs to exchange votes. Plasma also implements non-validating nodes, who do not take part in consensus. Instead, they follow the finalized chain from validators and provide RPC access to applications and users.

Execution Layer (Reth)

Plasma uses Reth (Rust ETH), an execution client built by Paradigm. Reth is a reimplementation of the EVM written in Rust. It processes transactions, executes contracts, and updates state. Plasma is EVM-equivalent, therefore every opcode and precompile behaves the same as on Ethereum mainnet.

Reth connects to PlasmaBFT through the Engine API. The Engine API enables:

The consensus client to submit new block proposals to the execution client for processing.

The execution client to execute transactions in the EVM, update state, and return the result.

The consensus client to request block payloads from the execution client when proposing new blocks.

Both components to synchronize and maintain agreement on which blocks are valid and finalized.

PlasmaBFT proposes and finalizes blocks, then passes them to Reth. Reth applies the transactions in order and updates the state root. This follows the same consensus–execution split that Ethereum introduced after the Merge.

Reth is built in a modular way. It separates the transaction pool, block building, execution, and storage into distinct components. The transaction pool holds pending transactions. The block builder selects transactions to include. The execution engine applies EVM rules to update state. Storage keeps track of account balances, contract code, and contract storage.

Reth also uses staged synchronization for downloading chain data. This means it processes headers, bodies, and state in stages, rather than all at once. The approach reduces memory and disk requirements and makes initial sync faster.

Plasma Native Features

Plasma integrates stablecoin-focused features at the protocol level. These include zero-fee USD₮ transfers, support for custom gas tokens, and confidential transfers (currently under development).

Before discussing zero-fee USD₮ transfers and custom gas tokens, it is important to briefly explain paymasters and EIP-4337.

Paymasters are smart contracts that enable flexible gas policies such as allowing applications to sponsor operations for their users (theoretically enabling free transactions), or accept gas payments in an ERC-20 (e.g., USDC) in place of the blockchain’s native currency. The paymaster smart contract was introduced originally in EIP-4337. At its base, paymasters improve onboarding, allow convenient gas policies, and give more programmability to transactions.

EIP-4337 introduces a model where user operations (UserOp) are handled separately from regular transactions. Bundlers collect these operations into blocks, and paymasters validate and sponsor gas under rules. Paymasters implement a validatePaymasterUserOp function to check eligibility, ensure bounded costs, and take responsibility for paying gas.

In Plasma, the paymaster model is used in two distinct ways: one for zero-fee USD₮ transfers, and another for paying gas with custom ERC-20 tokens.

Zero-fee USD₮ transfers

Plasma implements a protocol-managed paymaster based on EIP-4337. This paymaster only sponsors two methods: transfer and transferFrom on the official USD₮ contract. It cannot sponsor arbitrary calldata or generalized transactions. Gas for these operations is prepaid by the Plasma Foundation.

To prevent abuse, the paymaster enforces identity checks and rate limits. Only verified users can access this subsidy, and usage per wallet is capped. This ensures the free transfer mechanism cannot be spammed indefinitely. This was one of the preliminary concerns when Plasma announced free transfers. In theory, any transaction can be free, on any blockchain (assuming that there are no incentive issues for validators or miners), however gas fees apply due to concerns around spamming.

There is work in progress to reserve blockspace for these transfers. One proposed design is to tag eligible USD₮ transfers in the mempool and modify the block builder to allocate a portion of the block’s gas to them first; unused reserved space would revert to general transactions. Any EVM-compatible wallet can support these gasless USD₮ transfers without modification, and they are compatible with both EIP-4337 smart accounts and standard wallet flows.

Custom Gas Tokens

Plasma also allows fees to be paid in approved ERC-20s. This is handled by another protocol-operated paymaster. The process works as follows:

The user selects a supported token.

The paymaster prices gas using oracle data.

The user approves the paymaster to spend the token.

The paymaster pays consensus gas in the native unit while deducting the ERC-20 from the user.

The custom gas paymaster is distinct from the zero-fee USD₮ paymaster. The USD₮ paymaster subsidizes gas; the custom paymaster accepts ERC-20 tokens in place of gas. This mechanism removes the need for users to hold XPL. Initial support includes USD₮ and pBTC, with scope to add more tokens later. Only protocol-approved tokens are accepted.

Confidential Transfers

Confidential USD₮ transfers are still under research and not yet implemented. The intent is to offer optional privacy while preserving EVM compatibility and composability.

The design aims to support features like:

Hidden transfer amounts and recipient addresses.

Encrypted memos attached to transactions.

Flows from private to public and public to private.

Selective disclosure (for audits or regulatory compliance).

As the module is under active research, details are not finalized yet. The ultimate goal is that confidential transfers should act similarly to regular ERC-20 transfers at the user, application and wallet level, meaning existing contracts and wallets can interact with them transparently. In addition, the Plasma team wants to ensure that they are able to achieve this efficiently (low computation and gas cost), enabling optional usage. As of now, the team has outlined that they are exploring stealth addresses (sending funds to one-time derived addresses), memo encryption, indexing methods, and proof systems as possible approaches.

Plasma One

As we’ve discussed above, countries with weak currencies and strict capital controls individuals and businesses turn to USD-pegged stablecoins as a store of value. Rather than hold rapidly depreciating local currencies, people in economies like Argentina, Turkey, Lebanon, Venezuela, and Nigeria park savings in digital dollars, primarily USDT. In these environments, stablecoins function less as payment rails and more as digital savings accounts, offering a more stable alternative for preserving purchasing power. Typically, these users have preferred centralized exchanges for sending, receiving, and earning on their digital dollars.

However, there is also a growing market of more sophisticated users who want a self-custodied way to manage their stablecoins. Over the past year, we’ve seen a wave of crypto cards and neobank providers emerge.

Traditional neobanks like Revolut often aggressively flag crypto deposits and withdrawals or charge high fees and spreads. Meanwhile, most crypto neobanks and cards sit a step removed from DeFi, making it difficult to move funds in and out of useful ecosystems and products, missing out on yield, rewards and vaults. Plasma One enables Plasma to offer banking and payments that can effectively utilize DeFi protocols on the backend. Although the majority of emerging markets users will likely continue to use centralized exchanges to send and receive payments, we believe that Plasma One offers a potential alternative choice to these users, as well as offering a DeFi-integrated neobank to sophisticated users.

Stablecoin-Native Neobank

Plasma One is a non-custodial stablecoin-native neobank and card that brings saving, spending, earning, and sending into a single platform. The goal is to package core financial services around stablecoins into one application, allowing users to treat digital dollars as ordinary money.

A central feature of Plasma One is the ability to spend directly from a stablecoin balance while it continues to earn yield. Users can pay with funds that remain productive until the moment they are spent, with stated yields of 10% or more. In addition, purchases made with the Plasma One card generate up to 4% cashback (in XPL).

The card will be available globally through Visa’s network: in more than 150 countries. Transfers within the Plasma system are advertised as free, with users able to send USD₮ instantly without cost, although the company notes that third-party fees may still apply depending on the route.

pBTC

Overview

pBTC fits naturally within Plasma’s goal of becoming a crypto-first neobank (Plasma One), strengthening the platform in two key ways:

First, it introduces Bitcoin as a counterpart to stablecoins in payments and savings.

Second, it enables BTC to circulate on Plasma, where it can serve as collateral, facilitate transfers, and integrate across DeFi applications.

The primary value of BTC on Plasma lies in its role as collateral. Historically, users have wanted to maintain their Bitcoin exposure while accessing liquidity. With pBTC, users can post their BTC holdings and borrow stablecoins or other assets against them, creating capital they can spend or reinvest without selling their underlying Bitcoin position.

Users also seek ways to accumulate more Bitcoin, typically through custodial products like cbBTC or directly on the Bitcoin native chain. However, cbBTC requires users to trust Coinbase completely for secure reserve management and redemption guarantees, creating single-point-of-failure risk. This custodial control also introduces potential freezes or restrictions based on compliance or operational decisions. The native Bitcoin chain presents its own limitations, lacking support for DeFi that would enable lending, borrowing, or other programmable financial activities.

Beyond productive Bitcoin usage, pBTC gives users access to a harder monetary asset. Crypto has proven invaluable for people in countries with runaway inflation, capital controls, and poor central banking through digital dollar access. Bitcoin extends this concept, offering protection against monetary debasement even in developed economies. While the US dollar remains the dominant unit of account and medium of exchange, its purchasing power faces ongoing pressure from inflation. Concerns about high government debt raise questions about long-term dollar stability, as large debt loads typically require governments to raise taxes, cut spending, or accept higher inflation to erode the real value of their obligations. This risk of persistent inflation drives some savers toward assets that cannot be issued at will. Both Bitcoin and gold appeal to those worried about currency debasement because of their fixed or limited supply characteristics, positioning them as “hard” assets in an environment of monetary uncertainty

pBTC Mechanics

pBTC is designed to bring native Bitcoin onto Plasma’s without relying on centralized custody or fragmented wrapped assets. Unlike existing Bitcoin representations such as wBTC, which rely on custodians to issue per-chain wrappers, pBTC is implemented using LayerZero’s Omnichain Fungible Token (“OFT”) standard. This ensures that pBTC functions as a single asset with a unified supply that can move seamlessly across multiple LayerZero-connected chains, rather than existing as separate token contracts on each network. Notably, pBTC operates as a fungible ERC-20 token, but the OFT framework ensures that it can be transferred to other LayerZero-connected chains without requiring rewrapping or duplicating liquidity pools.

The architecture of pBTC consists of three core layers. At the custody layer, users deposit BTC into addresses controlled collectively by the system. Withdrawals are governed by threshold signatures (MPC/TSS), which prevent any single verifier from accessing the signing key. The verifier network forms the second layer. Each verifier runs its own full Bitcoin node and indexer, monitors deposits and withdrawals, and issues attestations once transactions have reached finality. These attestations are published onchain, and a quorum is required for action to proceed. Finally, the issuance layer handles the creation of pBTC. When a sufficient number of attestations confirm a deposit, the corresponding amount of pBTC is minted directly on Plasma and linked to the user’s mapped address.

Below is a simplified transaction lifecycle to illustrate how pBTC works in practice:

Deposits:

When depositing, a user sends BTC to a Plasma vault.

Each verifier independently observes the transaction on the Bitcoin network, confirms its finality, and broadcasts an attestation.

Once a supermajority is reached, Plasma mints pBTC to the user’s wallet.

Withdrawals:

For withdrawals, a user burns pBTC on Plasma and specifies a destination Bitcoin address.

Verifiers confirm the burn and collectively sign a Bitcoin transaction using MPC/TSS.

Only after a quorum is reached is BTC released back to the user on the base chain.

Although OFT still employs a burn-and-mint mechanism to preserve global supply, it differs from traditional bridges in a few important ways. Firstly, conventional bridges typically issue separate wrapped assets on each chain, fragmenting supply and liquidity. They also often rely on custodians or small multisigs to control locked collateral. In contrast, OFT treats the token as a single global supply and uses LayerZero messaging to transfer state between chains. Token issuers retain direct control of the contracts and configuration parameters, and the standard is designed for multichain use rather than retrofitted bridging.

Since pBTC exists as one unified supply across chains, liquidity is not fragmented across multiple wrapped versions. Withdrawals are secured through quorum-based threshold signatures rather than a single custodian, reducing unilateral control. In addition, all verification events are published onchain, making them auditable by any participant.

Tokenomics

Token Utility

XPL is the core asset securing the L1 via Proof of Stake (PoS) and is used to facilitate transactions as well as to reward those who provide network support by validating transactions. XPL safeguards the integrity of this new system and aligns long-term incentives as stablecoin adoption scales.

Token Supply

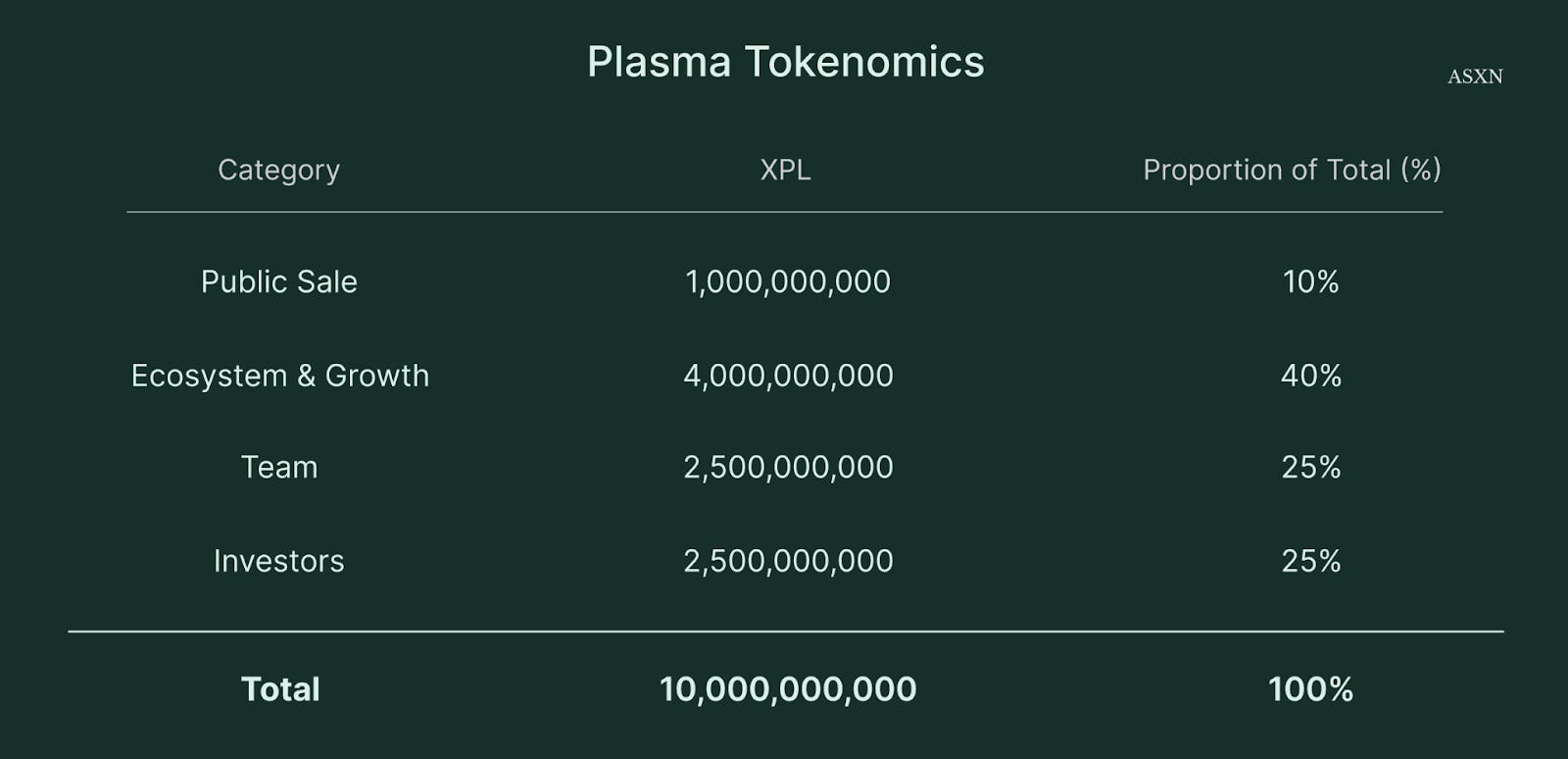

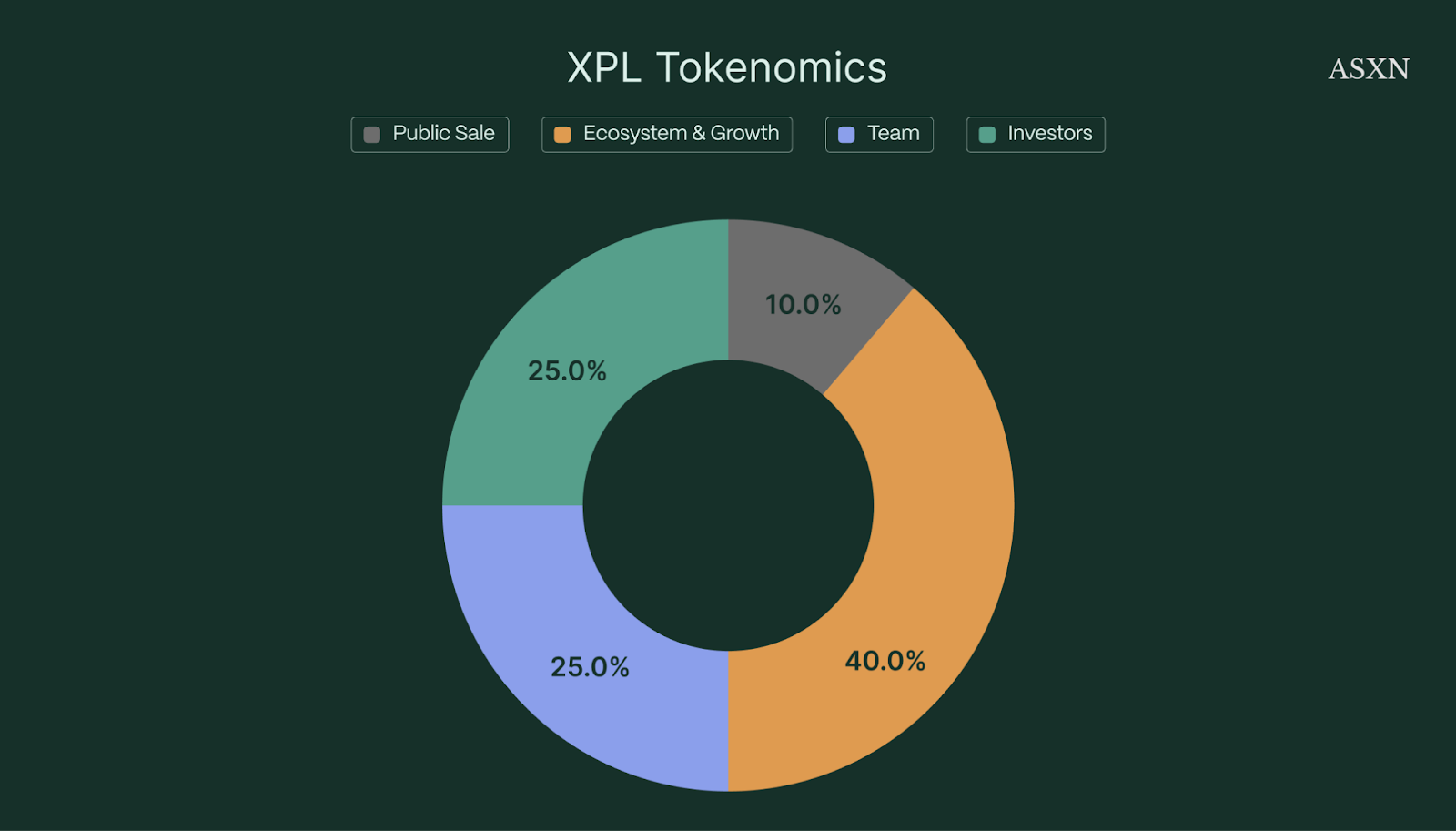

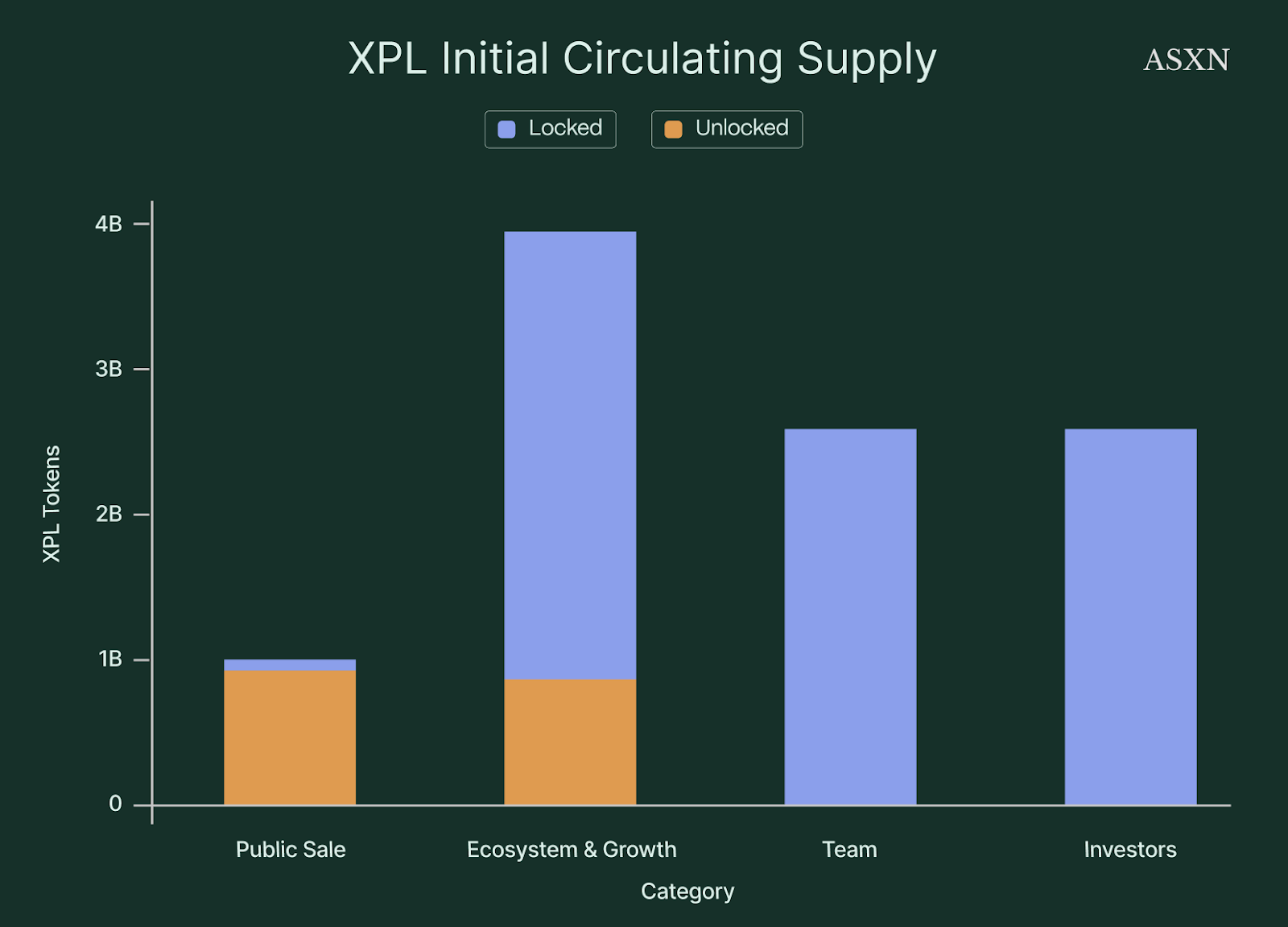

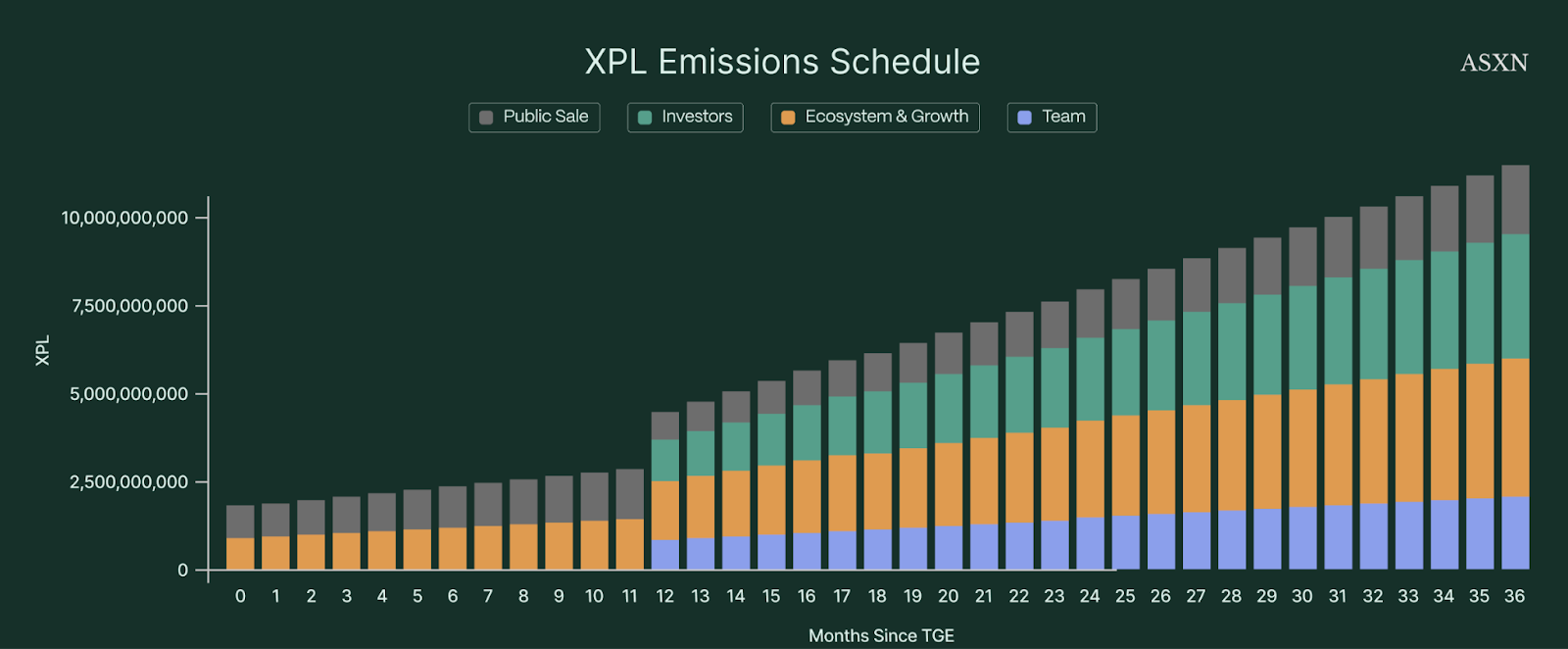

The initial supply will be 10B XPL at mainnet beta launch, with programmatic increases (inflation) for staking that will be introduced later. The initial XPL distribution is as follows:

XPL Public Sale (10%) - On May 27th 2025, the Plasma team announced the XPL public sale, where 10% of the XPL supply (1B XPL) was allocated to participants in the deposit campaign. $50M XPL was sold pro-rata at a $500M valuation to participants who deposited stablecoins into the Plasma pre-deposit vault. You can see the full vault data on our Dune dashboard. The XPL sold in the public sale are unlocked as follows:

XPL purchased by non-US purchasers are fully unlocked upon launch of the Plasma Mainnet Beta.

XPL purchased by US purchasers are subject to a 12-month lockup and will be fully unlocked on July 28, 2026.

Ecosystem and Growth (40%) - The Plasma team “plan to leverage XPL to intensify Plasma’s network effects, not just in crypto-native ecosystems, but across traditional finance and capital markets as well” and as such have allocated 40% of the supply toward strategic growth initiatives that are designed to expand the utility, liquidity, and institutional adoption of the Plasma network. These tokens are unlocked as follows:

8% of the XPL supply (800,000,000 XPL) will be immediately unlocked at Plasma’s mainnet beta launch to provide for certain DeFi incentives with strategic launch partners, liquidity needs, support exchange integrations, and to implement early ecosystem growth campaigns.

The remaining 32% (3,200,000,000 XPL) unlocks monthly on a pro-rata basis over the following three-year period, such that 100% of the Ecosystem and Growth allocation is unlocked on the date that is three years from the launch of the public mainnet beta.

Team (25%) - 25% of the XPL supply (2,500,000,000 XPL) to incentivize current and future service providers. In addition to vesting schedules tied to start dates, the XPL allocated to the team are unlocked as follows:

One-third of the XPL team tokens are subject to a one-year cliff from the date of the public launch of Plasma mainnet beta.

The remaining two-thirds are unlocked monthly on a pro-rata basis over the following two-year period, such that 100% are unlocked on the date that is three years from the date of the public launch of Plasma mainnet beta.

Investors (25%) -25% of the XPL supply was allocated to Plasma investors, both institutional and community with participation from Founder’s Fund, Framework, and Bitfinex, among others as well as the first Echo sale to private investors.

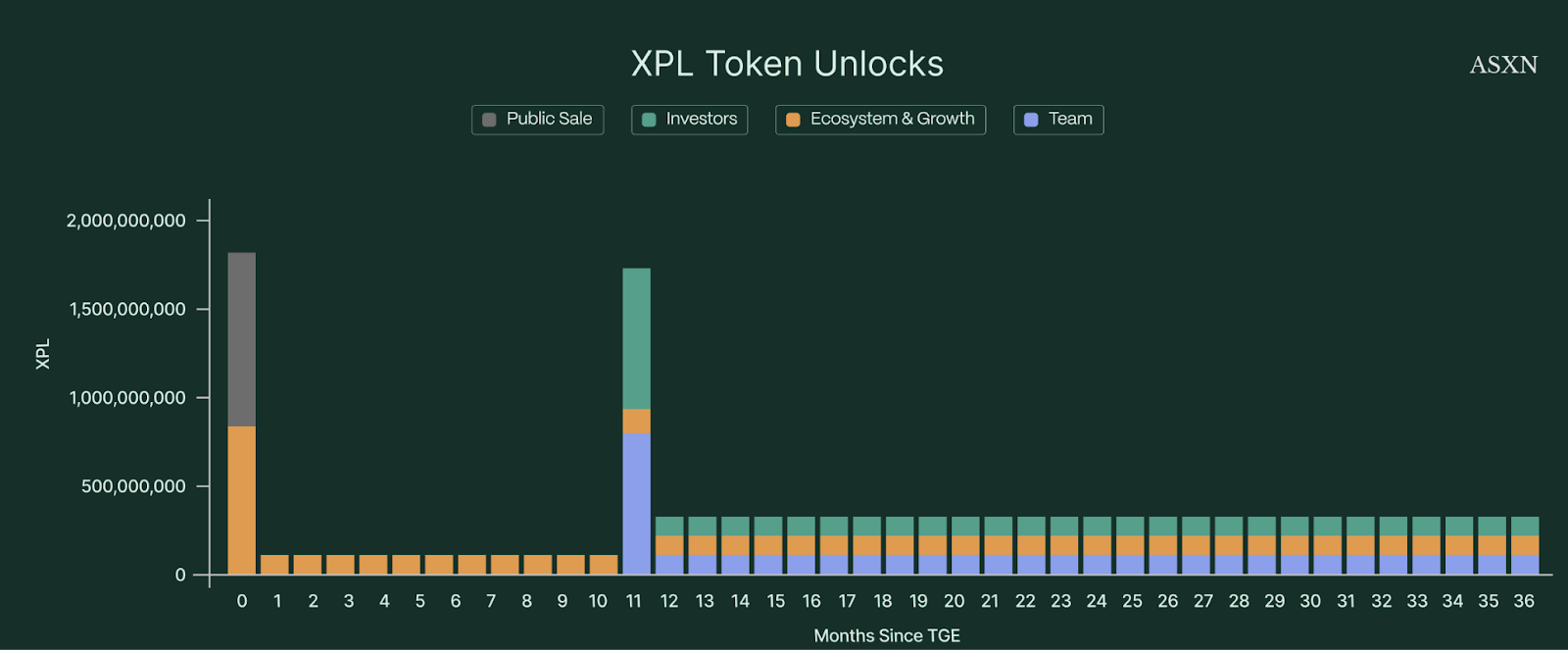

Emission and Inflation Schedule

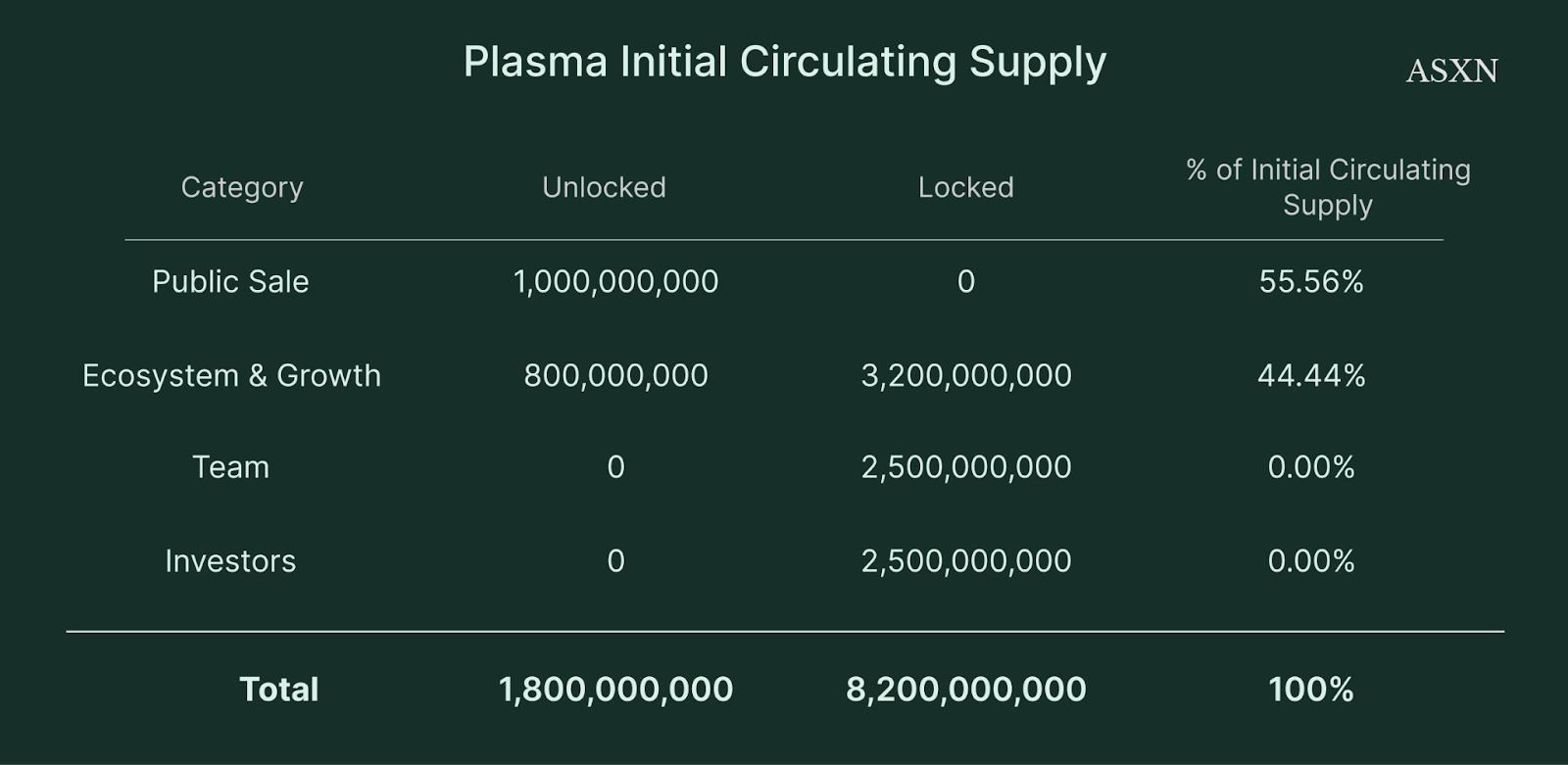

At TGE, the XPL token will initially only have ~18% of the total supply circulating, with the remaining supply locked up per the vesting schedules. The initial token supply will be coming from the public sale allocation and 8% of the total XPL supply from the ecosystem and growth allocation. Supply on TGE will look as follows therefore:

Note: this assumes 100% of the public sale was sold to non-US citizens and undergoes an immediate unlock on TGE. In reality, the initial circulating supply will be lower as any US citizen participating in the sale will be locked for 1 year. For example, if 10% of the sale was conducted by US KYC’d accounts then the initial TGE supply would be: 1B * 90% + 800M = 1.7B XPL.

In terms of vesting, both the team and investors follow the same path to liquidity, while the ecosystem and growth allocation unlocks gradually on a linear schedule over three years. The outcome is as follows:

Since Plasma is a PoS blockchain, validator rewards are typically minted by the protocol with two goals: (i) ensuring validator economics remain attractive to secure the network with top-tier participants, and (ii) minimizing long-term dilution for XPL holders. As such, XPL rewards begin at a 5% annual inflation, decreasing by 0.5% per year to a 3% baseline, and only activate once external validators and stake delegation are live.

Emissions are distributed to stakers via validators, with the locked team and investor XPL excluded from rewards. To offset dilution, Plasma adopts an EIP-1559 model, permanently burning base transaction fees: creating a balance between new emissions and network usage. More details regarding validator rewards will be published before inflation and rewards go live.

You can track all tokenomics, XPL emissions, XPL token burn and gas fees on our dashboard here:

DeFi

Plasma appears to have a three pronged growth approach to reach their end goal of settling more dollar transaction value than any other blockchain or payments company in the world. The below report dives into these three prongs:

Tapping Into Existing USDT Users:

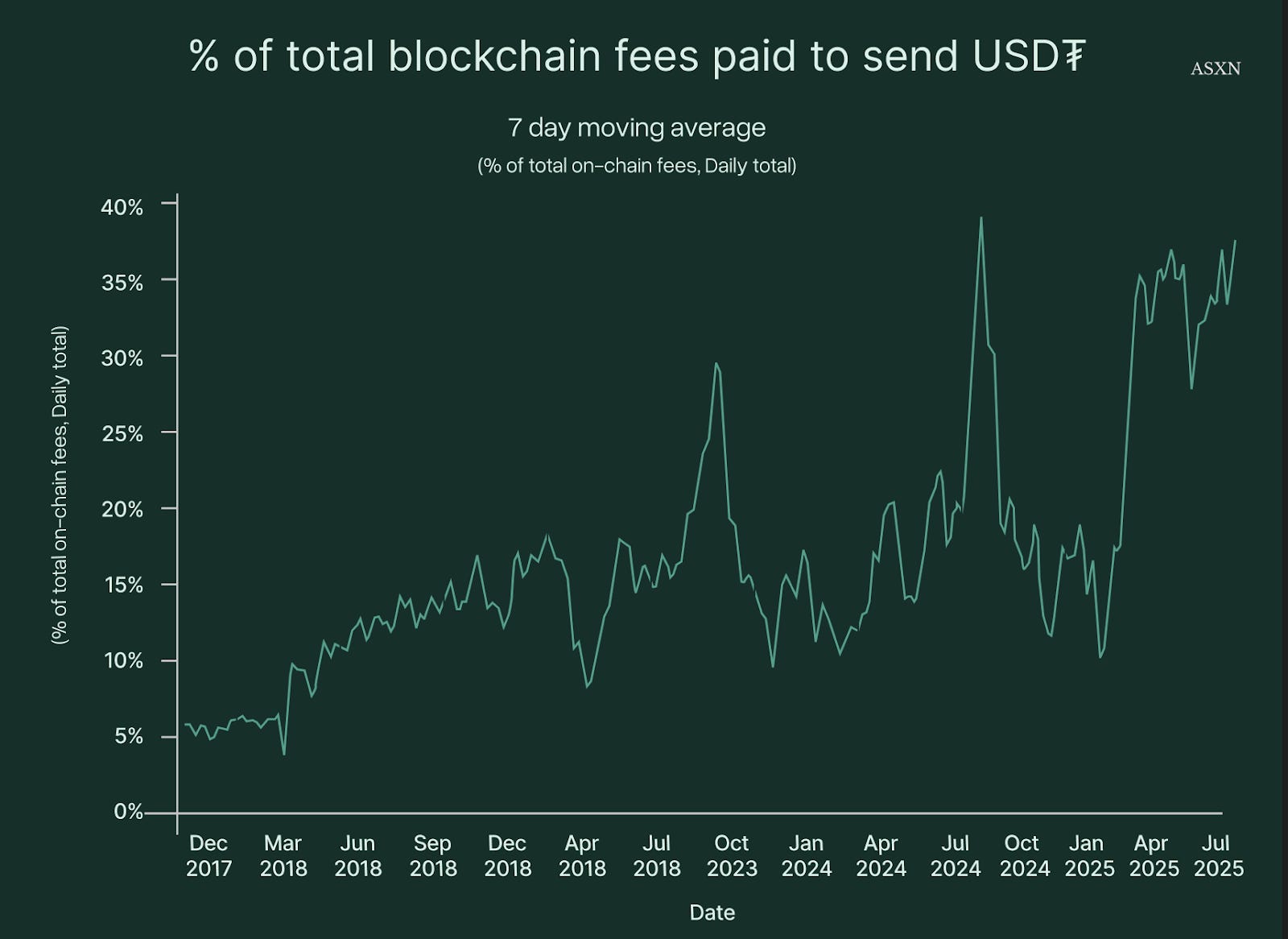

US Dollar Stablecoins are already a $292B market, up 69.7% YoY and 70x since the start of the decade. This is unfathomably quick growth, with all signs pointing towards multi-trillions in supply in the next several years. By offering zero fee USDT transfers, Plasma can quickly tap into the existing Tether supply ($170B) and take market share from chains that have failed to deliver a smooth user experience for people that just want to hold money, make payments and transfer dollars. Based on August 2025 Chainalysis data, 40% of all blockchain base fees were used for simple USDT transfers.

Growing The Pie and Onboarding Those With Broken Payment Infrastructure

Roughly 30% (2.4B people) of the world does not have access to basic, affordable financial services: which includes transactions, payments, savings and credit. While there is a clear learning curve to using stablecoins, it is likely the #1 easiest and fastest way to give people USD access to three of those four categories (credit still needs improvement). Distribution, UX and a broad ecosystem of financial primitives are the three things holding Plasma back from onboarding hundreds of millions of people to a less extractive and limited platform. Access to Plasma means self custody, access to a plethora of real world assets and 24/7 feeless transactions.

Onchain Economy for Crypto-Natives and Investors

Veda, Binance Earn and Maple brought in nearly $3B in USDT TVL on launch day. It will be completely dependent on Plasma to have a fully built out DeFi ecosystem that will enable this capital to be deployed at attractive rates, as well as attract the next hundred billion dollars to flow into the ecosystem. We will dive into Plasma’s Day 1 launch partners and explore how productive capital in crypto is currently deployed in the next section.

Having a L1 with many day 1 applications is clearly not a sufficient differentiator from competitors like Solana, Ethereum, Tron and Hyperliquid. Plasma’s opportunity is in offering the full end to end money experience, from getting paid, to paying your bills, to saving your money or making investments. The full end to end experience means that Plasma can find PMF not only with those lacking access to basic financial primitives, but also for crypto natives and a broader range of investors.

Other chains have made meaningful strides in terms of throughput and UX over the past 5 years, which is part of the reason we have seen tens of billions of dollars in stablecoin growth year after year. However, we firmly believe that the next several years of improvements across wallet security, smart contract resilience and quality asset issuance will be what is required to make stablecoins a $3T+ market and Plasma will be in a prime position to capture this growth.

We mentioned it in our first Plasma focused report, but the CEO of PayPal has focused on his platform’s inability to keep capital within their company’s system. In 2024, their 430M active users did 26B transactions totaling over $1.7T in volume, but far too often the receiving party of a PayPal transaction, whether P2P or P2B, immediately withdraws the cash into their bank account. This makes a lot of sense, given their users want to have tangible access to that money, where they can spend, earn interest / invest and pay bills. The below sections will cover Plasma’s plans to EVERYBODY access a best in class payments system (much like PayPal), but also have access to most of their financial needs on a single network.

Day 1 DeFi Ecosystem

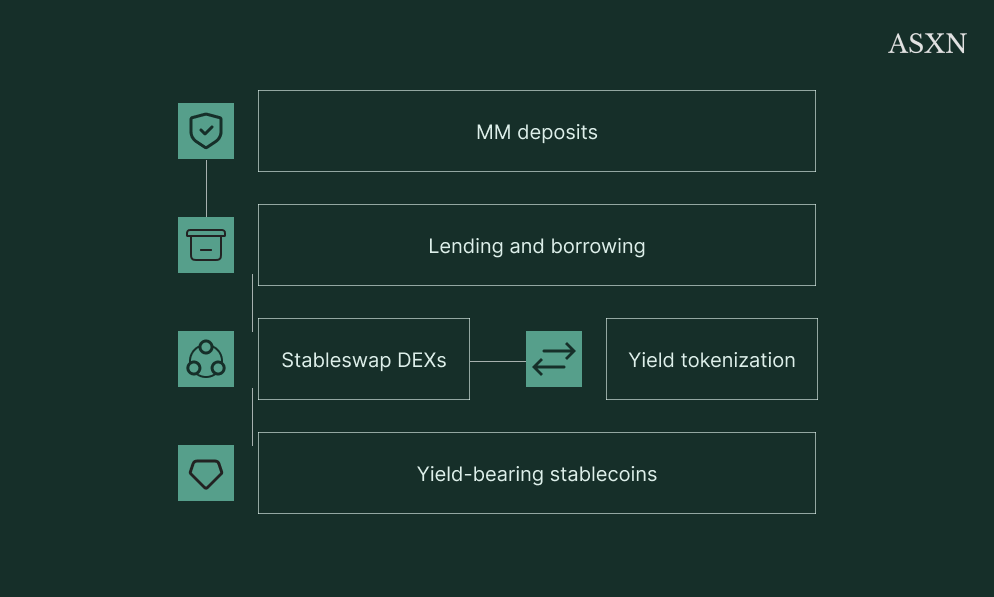

In the next several weeks, Plasma will be home to billions of dollars in USDT. The network has been designed top to bottom to attract stablecoin inflows, and then retain them. Over the last several weeks, we have seen Plasma partner with some of the most successful protocols across other ecosystems (Aave, Maple, Veda, Uniswap, Pendle, etc). Focusing on the core primitives with these day one launch partners should hopefully allow a very targeted DeFi incentives campaign and we see that “8% of the XPL supply (800,000,000 XPL) will be immediately unlocked at Plasma’s mainnet beta launch to provide for certain DeFi incentives with strategic launch partners, liquidity needs, support exchange integrations, and to implement early ecosystem growth campaigns.” So what is needed to create a self sustaining DeFi ecosystem?

Asset Issuance, Credit and Inflow Drivers

Beyond USDT, Plasma will support a broad range of longtail stablecoins and tokenized vault products, including notable launch partners like Ethena, Centrifuge, USD.ai, Neutrl, Resolv and Clearpool. Given a Day 1 Pendle integration, there are fairly large growth expectations for all of these assets on Plasma mainnet. Below is a spotlight on a few of the launch partners:

Ethena ($14B in TVL) will be live on Plasma at launch. Given USDe’s rapid growth, Ethena must continue to generate significant USDT / liquid stable deposits, on which they can earn yield and ensure withdrawals from the protocol can happen seamlessly without having to open and close positions at non-optimal times. This should be a black hole for hundreds of millions of dollars in USDT and BTC on Plasma

Binance Earn and Plasma are launching a campaign that will offer Binance’s 280 million users a chance to make their $30B+ of USDT productive within the Plasma ecosystem, where they will earn onchain yields and XPL incentives

Maple ($4B+ in TVL) launched a syrupUSDT vault that will bring $200m in deposits to Plasma at launch. The vault filled up immediately at launch, showcasing the high demand for XPL incentives and excitement to move stablecoins over to Plasma. Maple offers overcollateralized loans to crypto-native companies that need short term financing.

Centrifuge ($1.2B+ in TVL) offers onchain access to tokenized assets, specifically treasury and credit funds. These tokenized vaults offer basically unlimited exposure to 4-5% yields given the market depth of US Treasuries and the wider AAA bond market. This should be an amazing market for non-US investors to get access to some of the safest lending opportunities onchain.

USD.ai ($750m in TVL, $500m for Plasma) is a relatively nascent protocol that is financing hardware (GPUs) for AI companies. The borrower is able to tokenize these GPUs via a bankruptcy remote SPV and borrow from depositors of the USD.ai vault, compensating them at a rate several points above the risk free rate. Given AI’s growth over the last several years, we can predict that demand for GPU’s and the need to finance the actual hardware will continue growing exponentially. There are obviously different offchain risks here, but it is another liquidity sink for stablecoins chasing yield on Plasma.

There are a few, key prelaunch protocols, coming to market on Plasma that should get significant XPL incentives:

Axis is an onchain vault that allows depositors to enjoy the upside of price discrepancy arbitrage across different trading venues.

Daylight is a renewable energy company that looks to use the onchain economy to drive down the cost of solar installation and eventually create a marketplace for renewable electricity created on the decentralized grid.

Uranium Digital is a 24/7, institutional uranium trading platform.

The Plasma team plans to continue pushing forward sourcing credit opportunities to drive new opportunities for stablecoin holders on the chain in the coming months post launch.

Liquidity and Trading

If the Plasma vision comes to fruition, there will be thousands of stablecoins for different currencies, with different upsides and trust assumptions. Being able to swap assets or currencies with little to no price impact is hugely important in bringing high value users to the ecosystem.

At launch, Uniswap, Curve, Fluid and Balancer will be deployed with professional pool management to support stablecoin swaps, ensuring that users of the chain should be able to enter / exit stablecoins near their peg at all times. Plasma has offered to direct tens of millions of dollars in XPL incentives to different USDT pools over 6 months, making sure there is permanent liquidity against XPL, ETH, weETH, XAUT and then many of its longer tail stablecoins that we mentioned in the section above.

Read more about Plasma’s incentive offers in Uniswap’s governance forum.

Onchain Leverage

Plasma’s DeFi ecosystem has an important scale to balance, provide high enough yields for stablecoin holders to flock to the network, but also ensure that borrowers can find competitive rates such that they are also interested in participating in Plasma DeFi. The key will be to find other drivers of yield, outside of the demand for onchain leverage and to incentivize Aave deposits with enough XPL to make people move their positions over from Ethereum. We believe that the roll out of Ethena and Plasma One will both bring a massive amount of supply side liquidity to borrow / lend protocols. Ethena needs to make their stablecoin balance productive to prevent drag and Plasma One card users will be keen to earn 4-5% on their stablecoin balances - as Plasma’s DeFi lead said, “Borrowers, meet lenders.”

Aave ($69B in TVL), the most trusted onchain lending platform, will be there to support the DeFi ecosystem on Day 1. Euler, Fluid and Wildcat are also day 1 launch partners, who will bring permissionless markets, undercollateralized lending and other borrower centric lending features to the network.

Vaults and Yield Management

Yield management and actively managed DeFi vaults have grown significantly over the past couple of years and will play an extremely important role within the Plasma ecosystem, given the abundance of stablecoin supply. Pendle and Veda are two launch partners that bring a great deal of customization to generating yield within the Plasma ecosystem.

Veda: A non-custodial DeFi vault curation protocol for automating and optimizing onchain capital allocation.

Allows suppliers to passively earn best in class yield, without having to constantly manage their positions across dozens of protocols and keeps the DeFi ecosystem efficient and in balance as it attempts to deploy the passive capital to pools with the highest risk-adjusted returns at any given moment

Pendle: A tokenized yield trading platform that allows traders to speculate on future returns of yield bearing assets.

Pendle lets traders lock in a fixed return on a yield bearing asset by allowing speculator to buy the rights to the future yield, if they believe that the returns will be higher than the Pendle market is pricing

The combination of these two launch partners builds out the Plasma ecosystem for both the sophisticated / active trader and the more passive DeFi users that may be using Plasma for payments and savings. Combining best in class yield with a feature rich DeFi ecosystem gives Plasma a real chance at competing with some of the best layer 1s in crypto.

Thesis

Stablecoin Supercycle

Stablecoins are emerging as the foundation of a new financial system. They offer faster settlement, lower transaction costs, seamless cross-border functionality, programmability, and auditability. Their adoption has been rapid: as mentioned above, the market has grown from $30M in 2018 to more than $250B today, a CAGR of 263%. Initially, they were primarily used in crypto-native contexts: primarily by market makers and arbitrageurs as collateral and settlement assets, in DeFi collateral structures, or by exchanges for stablecoin-based margining.

However, their use cases have grown beyond crypto-native applications. Citizens in high-inflation or economically unstable economies increasingly use stablecoins as a store of value, while remittance markets are adopting them for low-cost, near-instant cross-border payments. This adoption has been supported by improvements in infrastructure, including efficient on- and off-ramps, cheaper chains, and better wallets.

The market is expected to continue scaling into the trillions of dollars. This is primarily as their growth also intersects with global macroeconomics: reserves backing stablecoins increasingly include US Treasuries, making stablecoin issuers a structural source of demand for government debt. At present, stablecoins collectively rank as the 15th largest holder of Treasuries, with about $193B of exposure.

Policymakers have begun to recognize their strategic role. Stablecoins are seen as tools to reinforce dollar hegemony, manage sovereign debt, and strengthen financial systems. In the US, bipartisan legislation is advancing to regulate issuance and reserves, with the House-led STABLE Act and the Senate’s GENIUS Act both establishing frameworks for compliant dollar-pegged stablecoins. These developments suggest that regulatory clarity is within reach, further enabling growth for stablecoins. Plasma is set to benefit from growth of stablecoins, as they are positioning themselves as a purpose-built, stablecoin-optimized chain.

Ethereum and Tron Are Not Purpose-Built

Most stablecoins currently sit on Ethereum and Tron, but neither chain was designed with them in mind. Ethereum suffers from prohibitively high fees (at peak times), while Tron combines significant fees with centralization. Both limit stablecoins’ potential to function as efficient money-transfer systems.

This opens space for purpose-built infrastructure. Plasma addresses these limitations by offering zero-fee USDT transfers. With an existing Tether supply of $170B, there is significant opportunity to capture flows from users who currently bear unnecessary costs. As of August 2025, 40% of all blockchain base fees were spent on simple USDT transfers. Plasma’s model directly targets this inefficiency, providing a smoother and more cost-effective experience for payments and transfers.

Crypto-Native Neobank

Plasma One is designed as a stablecoin-native neobank. It combines saving, spending, earning, and sending into a single non-custodial application, allowing users to treat stablecoins like ordinary money. This positions Plasma as a full-service financial platform rather than just a payments rail.

There is also a growing market of more sophisticated users who want a self-custodied way to manage their stablecoins. Over the past year, multiple crypto cards and neobank providers have launched to meet this demand. Traditional neobanks such as Revolut often flag or restrict crypto-related transfers, while also charging high fees and spreads. At the same time, most crypto-native neobanks and cards remain disconnected from DeFi, limiting users’ ability to move funds into productive ecosystems that provide yield, rewards, and vault strategies. Plasma One addresses these gaps by enabling banking and payments that connect directly with DeFi protocols on the backend. This allows users to retain custody of their assets while accessing a broader range of financial opportunities.

Stablecoins themselves unlock permissionless access to diverse yield-generating strategies. Returns can be generated from Treasury holdings, liquidity provision in stablecoin pools, lending markets, structured strategies such as perpetual futures arbitrage, and private credit markets.

Currently, DeFi is concentrated on Ethereum, which limits accessibility due to high costs and complexity. By contrast, onboarding DeFi into a neobank-tied L1 could simplify access, integrate financial services, and expand participation. Incentives in the early stages are likely to drive user capture. Plasma’s approach positions it to serve both sophisticated crypto-native investors and broader markets, combining traditional financial primitives with integrated DeFi yield in a single platform.

Payments and Remittances

Stablecoins provide an internet-native alternative for moving money. They settle in seconds, are available at all times, and cost far less than traditional systems. By comparison, the global average cost to send $200 abroad in late 2023 was 6.4%, with some corridors exceeding 10%. These fees act as a regressive burden on workers who rely on remittances. On public blockchains, transaction costs are measured in cents or fractions of a cent. For example, recent average fees on Base were just $0.00024, compared to $0.155 on Ethereum. Plasma intends to push costs even lower, with zero-fee USDT transfers.

Remittances are particularly important in emerging markets, where centralized exchanges are often the primary channels for sending and receiving money. Plasma’s integration with Binance directly taps into this behavior. Through a joint campaign, Binance’s 280M users will be able to deploy over $30B of USDT into the Plasma ecosystem, earning onchain yields and incentives while also benefiting from cheaper transfers. This creates a direct path to onboard emerging-market users who already rely on CEX platforms, while also potentially extending services through the Plasma One app.

The role of stablecoins in these markets goes beyond payments. With over 20% of the global population living under inflation rates above 6.5% and more than half experiencing worse inflation than the US, digital dollars have become grassroots savings tools. In countries like Argentina, Turkey, Lebanon, Venezuela, and Nigeria, individuals and businesses increasingly use stablecoins to preserve purchasing power against volatile local currencies. In these cases, stablecoins act less as transactional mediums and more as digital savings accounts.

Disclaimer:

The information and services above are not intended to and shall not be used as investment advice.

You should consult with financial advisors before acting on any of the information and services. Kairos Research, Kairos Research staff, ASXN and ASXN staff are not investment advisors, do not represent or advise clients in any matter and are not bound by the professional responsibilities and duties of a financial advisor.

Nothing in the information and service, nor any receipt or use of such information or services, shall be construed or relied on as advertising or soliciting to provide any financial services.